Did you know the average cost of repairing a flooded basement is over $40,000? Flooding is becoming more prevalent in Ontario, and more homeowners are at risk of costly water damage to their property. Floods in Ontario are the costliest natural hazard when it comes to property damage.

Being proactive and taking the necessary measures towards protecting your home, especially against flooding and water damage, not only keeps you and your family safe, but it can save you big on your home insurance!

Why does being proactive save me on my home insurance?

Insurance revolves around managing risk, so it’s important for individuals to take measures to minimize their exposure. From an insurance company’s standpoint, mitigating risk holds significant value. Your home insurance premiums are determined by the insurer’s assessment of your risk profile. By actively taking preventive actions against potential losses, you become eligible for lower insurance premiums.

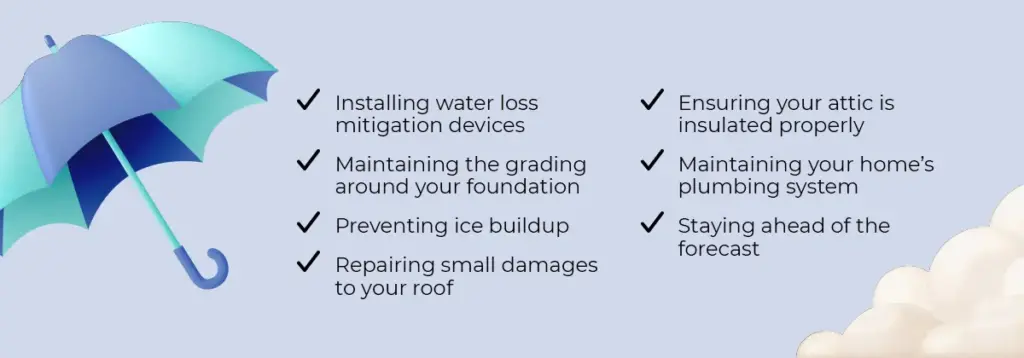

Here are a few examples of proactive measures:

- Installing water loss mitigation devices, like water alarms, backwater valves, sump pump backup, or water leak detection systems

- Maintaining the grading around your home’s foundation to ensure water is pooling away from your property

- Preventing ice buildup in your eavestroughs and gutters

- Repairing small damages or replacing missing shingles on your roof to prevent rainwater or spring melt from entering your home

- Ensuring your attic is insulated properly to guarantee adequate ventilation

- Performing regular maintenance on your home’s plumbing system

- Staying ahead of the forecast and surveying for heavy rainfall or other potentially damaging weather events

Purchasing water damage insurance is another way to be proactive against potential losses. While insurance does not substitute for the installation of water loss mitigation devices or good home maintenance practices it can serve as an additional layer of protection to save yourself the financial burden of having to pay for expensive home repairs or rebuild after a serious flood.

“Basic water damage insurance” is included in most policies, covering damages due to burst pipes, accidental escape from home water tanks, water infiltration due to another insured event (like a fire, impact from a vehicle, etc.), and sudden and accidental escape of water from municipal water mains. In addition to what’s already included in most policies, it’s recommended that policyholders strongly consider endorsements like sewer backup insurance, overland flood insurance, and groundwater insurance to cover against nearly all sources of water damage.

Sewer backup insurance

Sewer backup insurance is a cheap addition to any home insurance policy, although its cost can be greater if you live in an area that may be at higher risk of flooding. It’s designed to cover you for damage to your home because of unexpected sewer backup, whether from your septic tank, overwhelmed sanitary sewers, blocked gutter systems, or even blocked city sanitary mains.

Overland flood insurance

Overland flooding is considered one of Canada’s most frequently occurring natural hazards, consisting oftentimes of rainwater but it can also be mixed with chemicals and contaminants. Overland water insurance (or overland flood insurance) can cover you for the damages to your home because of unexpected overland flooding. It’s a bit more expensive than sewer backup insurance if you live in a higher risk area. Some areas that are at an extreme flood risk may not be eligible for overland flood insurance at all.

Groundwater insurance

Water damaging your home via seepage through basement walls, floors, and foundations can be costly, but it can be covered by groundwater insurance. Groundwater insurance, if available, provides coverage if water enters your home because of heavy rain, spring thaw, or the rising of the water table.

Municipal subsidy programs

Some cities in Ontario offer subsidy programs to help homeowners cover the cost of basement flooding mitigation devices. These may qualify you for an insurance discount, depending on what’s being installed to be proactive. For example, the city of Windsor offers a program with a lifetime eligible subsidy limit of $2,800 per property to install a backwater valve, sump pump, sump pump overflow, and/or disconnect foundation drains.

Keep in mind that water coverage in Ontario is ever-evolving as climate change continues to cause extreme weather events and municipal infrastructure proceeds to age. Discuss with your insurance broker to ensure you’re adequately protected against the risk of water damage.

Which insurance providers will discount me for installing water loss prevention devices?

Insurance companies like to see their policyholders taking proactive measures to mitigate loss. Here is a sampling of some of our insurance partners and the kind of water loss prevention devices they offer home insurance discounts for:

| Insurance Provider | Discount-Qualifying Water Loss Prevention Device |

|---|---|

| Aviva | Centrally monitored water alarm, sump pump backup, backwater valve, water alarm |

| CAA | Loss prevention device |

| Chubb | N/A |

| Commonwell | Ask a broker |

| Economical | Sewer backup and overland water loss mitigation sump pump alarm with automatic shut off |

| Intact | $1,000 towards installation of sewer back-up loss mitigation device at time of insured sewer backup loss |

| Pembridge | Water sensor and water prevention alarm |

| Portage | N/A |

| SGI | N/A |

| Travelers | Septic system credit |

| Wawanesa | Water leak detection (centrally monitored and mobile monitored) |

| 1Data source: Mitch insurance carrier partners | |

What should you do if you experience water damage in your home?

While insurance will help you in covering the cost of repairs/restoration to your home, it’s limited when it comes to physically protecting your property. If there’s been a particularly intense storm or heavy rainfall recently and water has gotten in your home, be sure to do the following:

- Shut off your water, ASAP.

- Move fabric, wood, or valuables off the floor to reduce the damage.

- Get you and your family somewhere safe if the issue escalates.

- Call your insurance company to report the loss.

- Once your home is safe to re-enter, document the damage as much as possible.

- Gather all receipts and proof of ownership to send to your insurer and hasten your claim.

While being proactive is always helpful in preventing a loss, it doesn’t 100% ensure you won’t experience water damage from an unexpected flood or storm. But with the right insurance in place, at least you know you’re covered.

Call a Mitch Insurance broker to discuss your current home insurance and see if you’re adequately covered against water damage.

Looking for home insurance?

Speak with a Mitch Insurance broker today to get a quote on home insurance in Ontario.

Call now

1-800-731-2228