Insurance 101 for eavestrough and siding contractors

December 16, 2024

The hailstorm in Calgary earlier this year caused nearly $2.8 billion in damage largely to automobiles and the roofs, siding, and eavestroughs of houses. The importance of contractors who specialize in fixing these damages cannot be understated, but contractors need protection, too! This is where having the right insurance comes in.

How exactly does business insurance work for eavestrough and siding contractors?

Insurance requirements for eavestrough and siding contractors

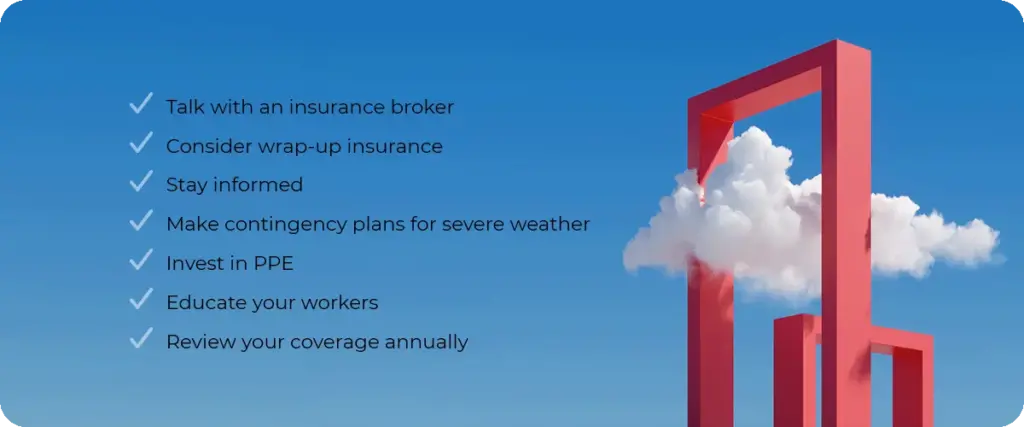

All contractors should protect their work with contractor insurance. It’s not necessarily a legal requirement, but it safeguards your business against financial losses and can also help you secure jobs and contracts. Clients want to be assured that the contractors they’re working with are adequately insured. That way the client isn’t left covering the costs if something goes wrong.

Contractor insurance isn’t always mandatory. It’s a recommendation, not a requirement, but it really should be a requirement given the extent of what you could lose in a lawsuit or if a severe storm hit your area! Some industries and regions will require to you to purchase insurance as well.

What coverages are needed for eavestrough and siding contractors in Ontario?

Siding and eavestrough contractors should take extra care in choosing a policy that provides appropriate protection. Without the right coverage, one simple mistake could leave you responsible for thousands of dollars in damages, potentially putting your finances and business at risk. But what coverage is needed? Well, here’s the basics of what is generally included in an insurance package for eavestrough and siding contractors:

Liability coverage

No matter how careful you are, there’s always a chance accidents could occur on a job site. Rather than facing the financial burden of being found liable for personal injury or property damage, choose an insurance policy that can protect you when incidents happen. Eavestrough and siding contractors insurance can include numerous forms of liability coverage, including:

- Premises liability

- General liability

- Personal injury liability

If someone trips over your equipment or you accidentally break a window, liability coverage will keep you from paying hefty costs out of pocket, protecting your livelihood and your reputation.

Property coverage

Installing siding and eavestroughing is a big job that involves a lot of tools and equipment. Don’t overlook safeguarding the investments you’ve made in all your important equipment. Whether your tools are on the job site with you, at your shop, or in your van, having the right property insurance will cover loss or replacement costs, keeping you ready to work without sacrificing time or money when damage, theft, or accidents happen.

Commercial vehicle insurance

As a contractor, you likely drive your personal vehicle to job sites. If you get into an accident or something happens to your car, truck, or van while on the job, your personal auto insurance may not be adequate. Commercial vehicle insurance expands your policy to include business use, providing coverage for repairs, property damage, replacement costs, and even injuries in the event of an accident. Whether you routinely transport tools and materials in your truck or simply use it to get yourself to job sites, having the right commercial vehicle insurance will make sure you’re protected on the road.

How much does eavestrough and siding contractor insurance cost?

Commercial insurance costs vary depending on the size and nature of your business. If you’re an independent contractor, you can expect to pay a lot less than if you were a huge company with multiple employees.

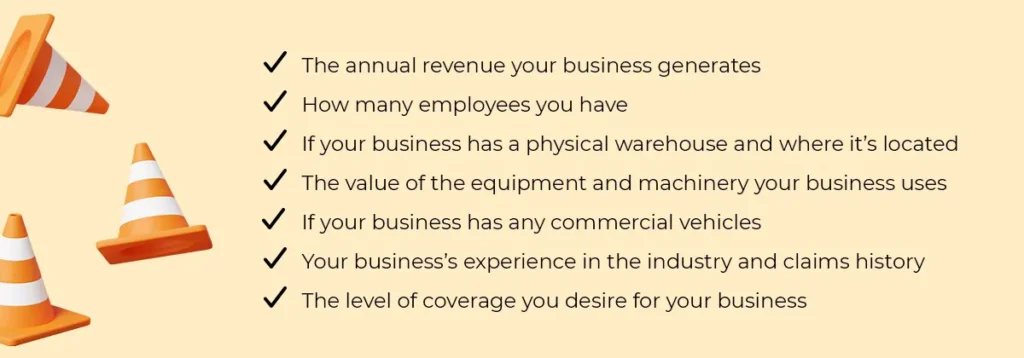

Here are some other factors that could influence the cost of your insurance coverage:

- The annual revenue your business generates

- anyhow many employees you have

- If your business has a physical warehouse and where it’s located

- The value of the equipment and machinery your business uses

- If your business has any commercial vehicles

- Your business’s experience in the industry and claims history

- The level of coverage you desire for your business

Costs can range anywhere from $50/month to over $200/month and beyond, depending on the scale of your business. To get an exact price for your operation, call us at 1-800-731-2228 for a free quote.

Does working in eavestroughing and siding call for specialized insurance?

All businesses have their own unique needs, and eavestrough and siding contractors aren’t exempt. Of course, there’s all sizes of eavestroughing and siding businesses – from large-scale companies to independent contractors. Depending on your operations, there may be a need for specialized coverages.

Our team of commercial insurance brokers take the time to learn about your business and can customize your policy to meet your exact requirements based on the specific risks you face.

Working as a self-employed contractor can be both challenging and rewarding and is well worth protecting yourself with the right contractor’s insurance in place. By choosing the best possible insurance for eavestrough and siding contractors, you can rest easier knowing your business is fully covered. Reach out for a free consultation and quote today.